Weighing CapEx versus OpEx for budget optimization

Key Takeaways

CapEx funds long-term assets that depreciate over years, while OpEx covers daily costs deducted in the same fiscal year.

The category you pick changes your tax bill, cash flow, balance sheet, and how investors read your company's growth story.

Most projects mix both: Hardware and licenses on the CapEx side, payroll, utilities, and subscriptions on the OpEx side.

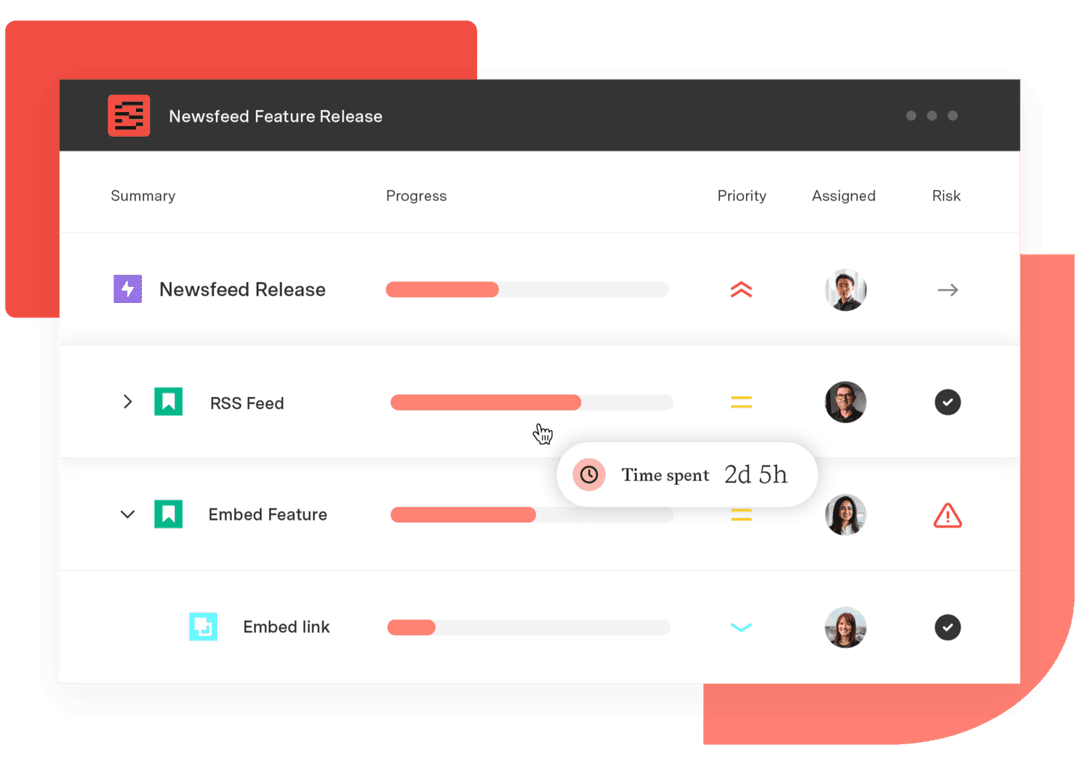

Track both in real time inside Jira with Tempo Financial Manager and Structure PPM so finance and delivery see the same numbers.

Capital expenditures (CapEx) are large, long-term purchases that benefit the business for more than one year and get depreciated over the asset's useful life. Operational expenditures (OpEx) are recurring day-to-day costs – payroll, rent, utilities, software subscriptions – that get expensed in the year they're incurred.

Project expenses tend to land in both CapEx and OpEx categories. How you split them out matters, because each type follows a different approval path, lands on a different financial statement, and tells investors a different story about how the company is being run.

Companies track both buckets to keep the books honest and make sharper budget decisions. You can quickly surface savings – especially on technology – by tightening up how you classify and report CapEx and OpEx expenditures. Flexera's 2026 State of the Cloud report has named cloud cost optimization as the top challenge for enterprise IT leaders across recent annual editions, a reminder that the OpEx column is now where most discretionary tech spend hides.

This is especially true with the explosion of generative AI; because most teams rely on usage-based LLM APIs and cloud GPU infrastructure, AI boom cycles are inflating the operational budget rather than traditional capital reserves.

What are capital expenses?

CapEx refers to significant, long-term projects or expenditures that, once implemented, improve an organization's fiscal performance, production capacity, or project quality. Unlike operating expenses, companies cannot deduct CapEx in the year spent; instead, they depreciate or amortize the cost over the asset's useful life.

These costs usually involve periodic, fixed spending on tangible assets like plant, property, and equipment (PP&E).

Capital expenses typically provide economic utility for longer than one fiscal year and are often the largest single line items a company commits to. The assets you buy represent your core business strategy and support long-term growth.

Typical CapEx expenditures include:

Manufacturing equipment

Facility additions and upgrades

Computer and network equipment

Company vehicles

Heavy equipment and machinery

Capitalized software development and major IT infrastructure

For a deeper look at how teams handle the project-level side of this, see Tempo's guide to CapEx tracking in Jira.

What are operational expenses?

OpEx covers all the recurring day-to-day spending required to keep a company functioning. These are the costs of doing business – the line items that help the organization manufacture goods, offer services, or attract customers. The benefits from these expenses are near-term, meaning you feel the impact of the OpEx budget within a fiscal year. Because they're tied to the current year's operations, these costs are usually fully deductible in the same fiscal year, immediately reducing taxable income.

Common OpEx expenses include:

Property or facility rent

Utilities

Payroll and salaries

Overhead costs

Property taxes

Research and development (R&D)

SaaS subscriptions and cloud hosting fees

Generative AI enterprise subscriptions and usage-based API token fees (LLM inference costs)

Note that under US GAAP (ASC 730) R&D is treated as OpEx, while under IFRS (IAS 38) research costs are OpEx but development costs can be capitalized as CapEx if they meet strict recognition criteria.

The shift to subscription software and cloud services has pushed a meaningful share of what used to be CapEx (servers, perpetual licenses) into the OpEx column. That matters when you're reading old benchmarks: A company that looks "asset-light" today may simply be paying for the same capabilities monthly.

CapEx versus OpEx: 7 key differences

It's not always simple to delineate between capital expenditures and operating expenses, but the two have very different impacts on budgeting, reporting, and cash flow. Here are seven crucial differences:

1. Size

While both expenditures improve a company's operations, they differ in the scope of their impact. OpEx spending covers the daily, weekly, monthly, and annual expenses that keep the lights on and the doors open. CapEx spending involves large costs expected to impact the organization's long-term capacity and profitability.

2. Timeline

A CapEx expenditure incurs an upfront payment, usually from a fund dedicated to PP&E purchases. OpEx items recur, so you'll generally pay them weekly, monthly, or annually.

3. Approval

Because of their size and the high initial disbursement, companies treat CapEx projects as high-stakes decisions they can't reverse. Before committing, CapEx planning requires rigorous business case development, research, and analysis, plus multiple levels of individual and panel approvals.

OpEx spending is a recognized business necessity affecting only the short term, so it rarely needs the same approval gauntlet. Managers usually review operating expenses at year-end to forecast next year's budget and flag any spending outside the historical norm.

4. Control

Companies typically purchase a CapEx asset outright, so teams control its operation and maintenance. That ownership lets them customize equipment to suit their needs, and if there's an in-house team handling upkeep, the company can reduce the operating cost by not contracting out to a third party. If a company leases technology or property as an OpEx expense, it gives up that control but also avoids the service and support burden.

5. Accounting

How accounting handles capital versus operating expenses is the biggest difference between the two. CapEx projects aren't tax deductible in the year spent and are included in the company's cash flow statement for the period the team expensed the cost.

If the newly acquired asset is tangible (like a new piece of equipment), its value depreciates over time. The company can claim the depreciated value after a waiting period as a tax deduction. If the asset is intangible (like a patent or license), the cost is amortized over the asset's economic life cycle. Amortization is deductible, reducing the company's overall tax liability.

Accounting strictly tracks asset purchase and depreciation, giving stakeholders and investors a clear picture of the organization's financial well-being. OpEx items get deducted during the period incurred, with teams expensing these items and including them on the income statement.

6. Budgeting

Companies fund capital and operational expenses differently, creating a dedicated pool to finance CapEx projects and using general funds for OpEx items.

Because CapEx projects involve a significant initial investment, companies typically approve only a few initiatives a year. CapEx budgeting usually means:

Creating a separate capital expenditure budget

Soliciting input at the departmental and organizational level

Setting a budget limit

Assessing every CapEx project's potential return on investment (ROI)

Companies build an operations budget by reviewing historical budgeting data and adjusting for inflation, creating a forecasted cost for the upcoming year. This information provides insight into projected revenue and profit for the next quarter or year.

Budgeting for OpEx items includes:

Historical trend analysis

Market trend analysis

Inflation rate review

For teams that want a repeatable model, Tempo's guide to project budget tracking walks through how to combine historical data, real-time spend, and milestone tracking inside Jira.

7. Investment

CapEx and OpEx give investors different perspectives on a company's financial health. Comparing CapEx to operating cash ratios lets stakeholders see how much money a company dedicates to capital expenditures. A high ratio reflects significant growth objectives, while a lower value suggests the company has matured.

OpEx analysis helps investors understand how an organization distributes its budget and allocates funds. Comparing OpEx against net sales showcases management effectiveness, providing insight into sales performance and revenue.

Some projects involve both CapEx and OpEx items. If a company establishes a data center, the building, networking infrastructure, and office equipment are capital expenditures. But the money it spends on office supplies, utilities, and coffee and snacks counts as operating costs.

How to balance CapEx and OpEx budgets

Most companies budget for both, but it can be hard to choose which to prioritize for a given project or company goal. A few things to weigh when deciding:

Financial strength: Owning capital assets means you don't have to keep paying for valuable equipment, which can improve your business's financial position.

Taxes: As an asset's value decreases over time, it produces a tax benefit when you claim it as a depreciation expense at year-end.

Investors: Reporting capital assets on the balance sheet signals higher profit and asset value to investors and other key stakeholders.

Potential losses: A company can't replace or walk back a capital investment without incurring significant losses. If you expect substantial growth or technological change in the coming years, an OpEx option is often safer.

Costs: Because of the upfront investment, CapEx projects require accurate projections, careful budgeting, and precise project cost tracking.

Return on investment: Estimating future requirements and the rate of technological change is essential to extending an asset's ROI.

A practical rule of thumb: If the technology is changing fast or the requirement may evaporate within a year or two, lean OpEx. If the asset is core to how you operate and you'll still need it in five years, CapEx wins.

Common mistakes when classifying CapEx and OpEx

The accounting rules look clean on paper. In practice, four mistakes show up over and over.

Capitalizing the wrong costs

Some teams try to capitalize software, consulting time, or maintenance work that should be expensed. Capitalizing too aggressively inflates current earnings and creates an audit problem later. The test is whether the spend creates a new asset or extends an existing one's useful life – if it just keeps the lights on, it's OpEx.

Treating cloud and SaaS as CapEx

Subscription software is almost always OpEx, but the line gets blurry on cloud implementation work. Under ASC 350-40 (as amended by ASU 2018-15), companies are required to capitalize implementation costs incurred during the application development phase of a hosting arrangement – custom configuration, coding, and system integration work – and amortize them over the term of the hosting contract. The mistake is capitalizing the wrong phases: training costs and post-go-live support must be expensed as incurred. Misclassifying those phases inflates the balance sheet and creates an audit problem later.

Check the accounting standard that applies to you (ASC 350-40 in the US for internal-use software, IFRS for international) before booking cloud spend as a capital asset. The same caution applies to AI initiatives: While building and training a proprietary model in-house might involve capitalizable internal engineering labor, the ongoing costs of running day-to-day AI queries and prompt inference are strictly operational.

No project-level visibility

Categorizing spend at the GL level isn't enough. If you can't trace CapEx and OpEx back to specific projects, you can't tell finance which initiatives are eating the budget. Project-level tracking is what turns the classification into a planning tool.

Forgetting the labor side

Internal engineering time spent building a capital asset can sometimes be capitalized, but most teams either miss the opportunity or capitalize hours that shouldn't qualify. Get a written policy, get finance and tax to sign off, and track those hours separately from regular operational work.

Project cost tracking with Tempo Financial Manager

Whether you need to monitor a single CapEx initiative or keep tabs on an entire portfolio of OpEx work, Tempo Financial Manager and Structure PPM give you real-time cost visibility right inside Jira.

Use Financial Manager to track budgets, expenses, and profitability, and rely on Structure PPM for live, roll-up views of scope and schedule that keep every stakeholder informed. For teams that want forward-looking numbers, project cost forecasting inside Financial Manager combines actuals, planned work, and budget data so you see overruns coming before they hit the books.

Sign up for a demo

Request Demo